Fixed Income Quarterly - Q2 2025

Macro-Economic Overview

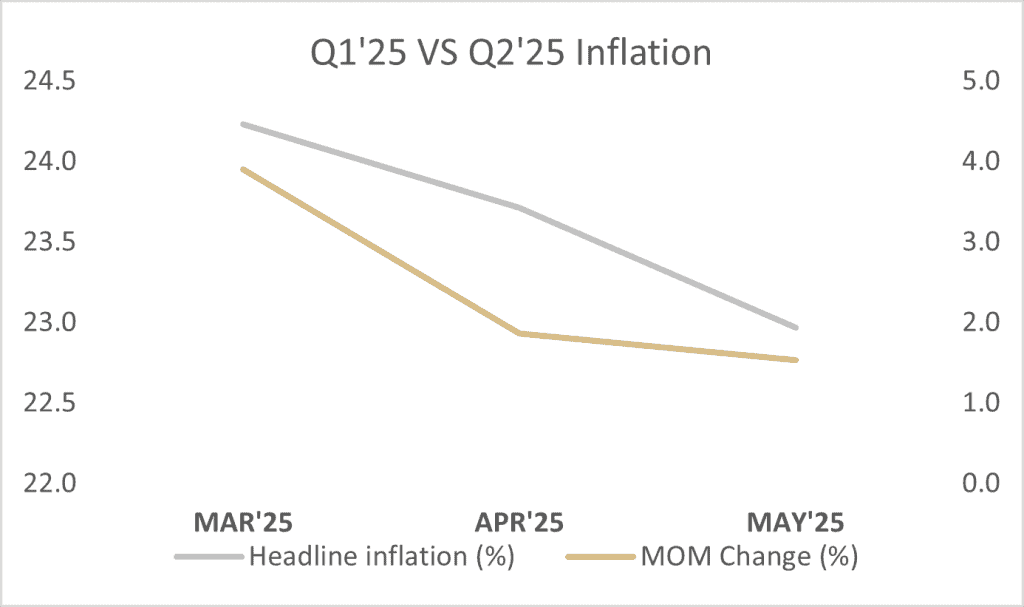

- Consumer prices continued to ease in May, printing at 22.97% YoY compared to 23.71% YoY in April 2025. The slowdown fed off the sustained downtrend recorded on the Month-on-Month CPI up to May 2025, as it came in at 1.53% M-o-M, which pales when compared to 3.9% MoM and 1.86% MoM in March and April, respectively.

- The composite Purchasing Manager’s Index (PMI) posted 52.1pts in May 2025, a continuation of the sustained expansions that has characterized aggregate economic activities in 2025.

- With the sustained expansion in real economic activities and the ease printed on the CPI, the Monetary Policy Committee (MPC) continues to hold Monetary Policy Rate (MPR) which remains at 27.5% and other policy parameters constant.

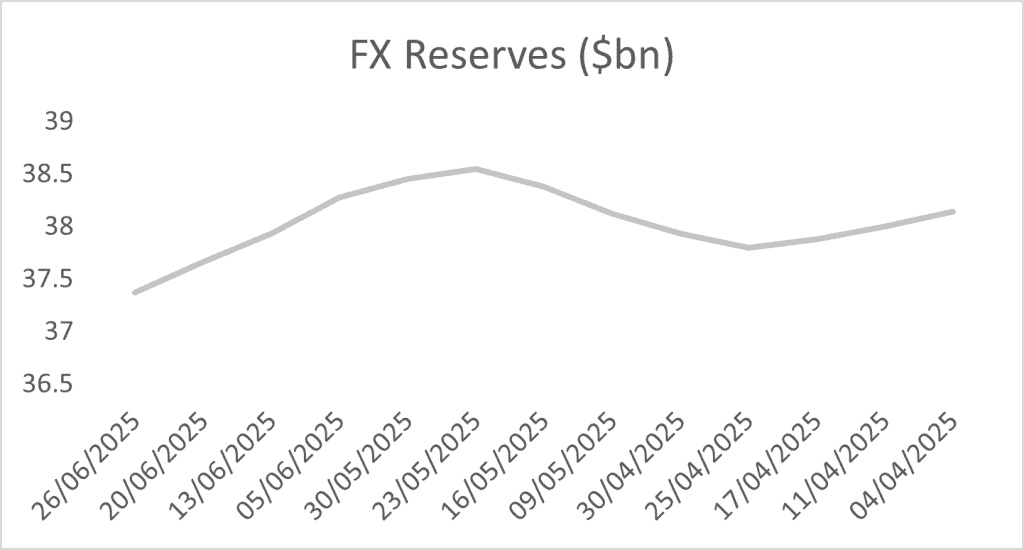

- External Reserves declined to 37.37 billion US dollars as of June 26, from 38.81 billion US dollars at the end of Q1.

- Amidst global uncertainty following US recent trade policies and the war between Israel and Iran, crude oil price has remained volatile through Q2 2025. In the period, the commodity posted high, low and average prices of $82.45, $63.16 and $70.77, respectively.

- The Total FAAC disbursement for the quarter stood at c.N4.918 trillion with May recording the highest at c.N1.618 trillion.

- Interbank Liquidity averaged N812.26 billion during the quarter. Liquidity was at a peak of N2.30 trillion and a low of N179 billion REPO in the quarter.

Bond market

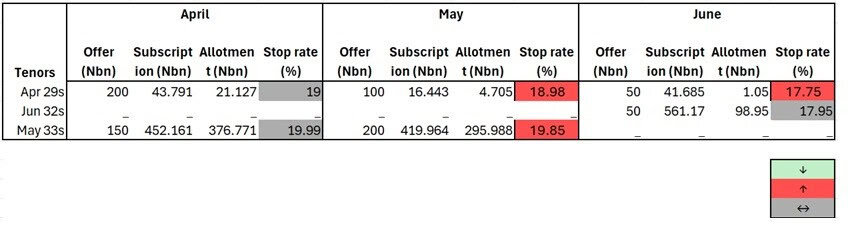

The FGN Bonds space in Q2 2025 was largely driven by bearish sentiment, as investors maintained a cautious stance amid heightened uncertainty around market direction at the start of the quarter. This lack of clarity contributed to a weak appetite overall, which pushed average yields up 24 bps to close at 18.67% in April. Midway through the quarter, the DMO issued a 7-year Sukuk at 19.75%, which prompted few sell-offs on existing Sukuk holdings, as investors sought to free up liquidity for the new issuance. Consequently, bearish sentiments persisted in the period as investors sought attractive deals. By late May, offers improved on the mid-dated bonds, with cherry-picking across the board emerging. As June commenced, the DMO announced the continued reissuance of the April 2029 bond, as well as the issuance of the new 7-year bond, prompting investors to position ahead of the auction. Following the auction, where the newly issued 17.95% June 2032s were tightly allotted, we saw strong bearish sentiments, with limited offers to match. Ultimately, post auction, June took a somewhat different trajectory as a result of exceptional demand at the Bond auction (N602bn over the N100bn offered), as well as the unmet demand trickling into the secondary market, ample liquidity in the system and improving economic sentiments, particularly the stabilization in inflation, all contributing to average yields declining by 63bps in June, closing the quarter at 17.97%. QoQ yields declined by an average of c.70 bps across the curve.

The DMO offered a total of N750bn at the bond auctions for the quarter across the April 2029s, June 2032s and May 2033s; c. N798.6bn was sold through the quarter (vs. N1.54trn subscription), with stop rates closing the quarter at 17.75% and 17.95% on the Apr 2029s and Jun 2032s respectively.

Treasury bill market

The quarter started with a slight liquidity squeeze, as prevailing economic uncertainty dampened investor confidence. Despite this, there was selective demand on the mid- to long end of the curve, with the long-end bill trading at an average yield of 23.58%. As a result, the average yield rose by 10 bps to close at 21.11% in April. As the quarter progressed, uncertainty persisted, although overall economic sentiments began to improve, aided by the rebasing of inflation by the NBS, with headline inflation easing to 22.95% in May. With system liquidity remaining elevated and the monetary policy rate held steady, bearish sentiment persisted on the mid- to long end of the curve. At the second auction in May, the auction subscription was 2.34x of the offer amount, reflecting robust investor appetite. This drove average yield down by 7 bps in May. As of 3rd June, system liquidity stood at N773bn, supporting further yield moderation in the primary market, which was mirrored in the secondary market. The gradual drop-in rates led to moderately bullish sentiments by month’s end. Thus, average yields on treasury bills fell by 93 bps, closing the quarter at 20.25%.

The CBN floated eight OMO auctions during the quarter, offering c.N4.5trn across the standard tenors. Sales throughout the quarter were about N7.12 trillion despite one no-sale auction being recorded.

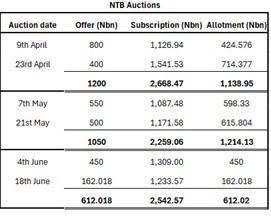

The DMO conducted six auctions through the quarter, with each month recording about 2.3x, 1.9x, and 4.2x oversubscription, respectively. In total, the FG oversold only c. N164bn across the standard tenors. Stop rates at the last auction of the quarter closed at 17.80%, 18.35% and 18.84% after 91, 182 and 364 days, respectively.

Eurobond Market In Q2 2025, the Sub-Saharan Africa (SSA) Eurobond market navigated a dynamic yet cautiously optimistic landscape shaped by persistent global headwinds and notable domestic policy actions. Investors grappled with the ongoing U.S.–China tariff war and volatile commodity markets, even as signs of stabilization emerged. Key SSA economies sustained or deepened reforms initiated in the previous quarter, striving to strengthen macroeconomic fundamentals against a backdrop of external uncertainty. Eurobond yield movements reflected this push-and-pull: initial risk aversion early in the quarter gave way to selective rallies in June, as markets digested easing inflation in several SSA countries and potential relief in global trade tensions. Overall, Q2 2025 proved to be a transitional period wherein global shocks were met with measured policy responses across the region, setting the stage for what could be a more stable second half of the year. Global Economic Factors Q2 2025 was marked by the escalation of international trade tensions alongside mixed economic signals from major economies. The U.S. administration’s tariff war with key trading partners entered a new phase: after imposing steep tariffs in January, President Trump maintained a hard line through Q2, raising levies on Chinese goods to “eye-watering levels,” which prompted equal retaliation from Beijing. These tit-for-tat measures rattled financial markets and threatened to upend supply chains. However, toward the end of the quarter there were glimmers of a negotiated respite – U.S. officials hinted at progress on trade deals (for example, resolving disputes over Chinese rare-earth exports) even as a looming early-July deadline for another round of tariff hikes kept uncertainty high. Investors remained wary but grew cautiously optimistic that some compromise might avert the most severe trade disruptions. Meanwhile, the U.S. economic outlook softened , reinforcing a more dovish tilt in monetary policy. Notably, U.S. GDP contracted by 0.5% in Q1 2025, the first quarterly decline in three years, as businesses front-loaded imports ahead of tariff implementation, underscoring the drag from trade policy uncertainty. In response, the Federal Reserve maintained a steady policy rate through Q2, holding its benchmark rate unchanged for the fourth consecutive meeting. This pause in U.S. tightening, combined with expectations of possible rate cuts later in the year, provided tentative relief for SSA issuers by tempering global financing costs. Indeed, the U.S. dollar weakened in late Q2 as traders bet on Fed easing amid the tariff standoff and mounting fiscal strains in Washington. China’s economic performance in early 2025 offered a mix of encouragement and caution for SSA commodity exporters. Official data showed China’s GDP grew by 5.4% y-o-y in Q1, slightly above expectations, thanks to solid consumer spending and industrial output. However, analysts widely downgraded China’s growth forecasts for the remainder of 2025, warning that the unprecedented U.S.–China trade war could sharply erode momentum. The impact of China’s slower-than-anticipated recovery was evident in global commodity markets: demand for raw materials remained subdued, applying downward pressure on prices of oil, metals, and other exports crucial to African economies. Commodity price volatility in Q2 was further exacerbated by geopolitical events. A brief but intense conflict in the Middle East – a 12-day war ignited by strikes on Iran’s nuclear facilities in mid-June, sent oil prices surging above $80 per barrel in a matter of days. This price spike provided a windfall for oil-exporting SSA countries (offering short-term fiscal breathing room) but simultaneously strained oil importers with higher energy costs. Fortunately, a swiftly brokered ceasefire brought relief: by the end of June, Brent crude had retreated to the mid-$60s. The supply risk premium ebbed as OPEC+ signaled modest output increases and U.S. shale production hit record highs. Nonetheless, the quarter’s oil price whipsaw underscored the fragility of market sentiment amid geopolitical flare-ups. Other key commodities showed mixed trends; for instance, copper prices remained elevated (around $5.0/lb in late Q2) as global investors positioned for long-term supply deficits, even though near-term demand from China was lukewarm. Taken together, these global factors: trade war jitters, a pause in U.S. rate hikes, China’s moderated rebound, and commodity swings due to conflict , created a complex external backdrop for SSA Eurobonds. Investors spent much of Q2 2025 recalibrating risk premia: early in the quarter, heightened trade and geopolitical risks pushed emerging market yields higher, but by June some stability returned on hopes of trade concession and accommodating central banks. This environment rewarded differentiation, as countries with improving fundamentals attracted renewed interest despite the global turbulence. Country Event Nigeria Nigeria’s economic trajectory in Q2 2025 was defined by macroeconomic consolidation and cautious monetary stewardship , which helped reinforce investor confidence in its Eurobonds. Following the CPI rebasing in January, which had recalibrated headline inflation from ~34% to 24.5%, inflation continued to trend downward through the second quarter. Headline CPI eased to 23.7% in April and 23.0% in May, aided by base effects, a stable exchange rate, and moderated food price growth. In response to this gradual disinflation, the CBN maintained a tight policy stance but refrained from any further rate hikes. At its May 19–20 meeting, the MPC voted unanimously to hold the benchmark interest rate at 27.5% , extending the status quo from earlier in the year. Instead of rate moves, the CBN relied on open market operations to manage liquidity: a series of OMO bill auctions in April absorbed excess naira liquidity, even as they attracted robust investor demand. These operations contributed to a rise in Nigeria’s external reserves , which climbed ~3% to reach $38.9 billion by mid-May, equivalent to about 7.6 months of import cover. This reserve uptick, bolstered by improved oil export receipts during the brief price spike, provided an extra cushion for debt service and currency stability. On the fiscal front, Nigeria intensified efforts to broaden its revenue base and reduce its historic reliance on oil. A landmark initiative to transform tax administration across all tiers of government, four tax bills, was signed into Law. Eurobond investors welcomed these developments. Secondary-market yields gradually narrowed by an estimated ~50 basis points over the quarter, reflecting improved inflation readings and reform-driven optimism. That said, investors remained vigilant toward Nigeria’s exposure to external shocks, such as any renewed oil price volatility or spillovers from the U.S.–China trade dispute, which could yet sway risk sentiment. Overall, Nigeria’s Q2 performance struck a positive note: prudent monetary policy, easing inflation, and proactive revenue reforms collectively underscored the country’s capacity to navigate a challenging global environment while steadily improving its macro fundamentals. Ghana Ghana’s Eurobond narrative in Q2 2025 centred on monetary policy prudence and encouraging signs of macroeconomic stabilization , even as the country continued to work through the aftermath of its recent debt restructuring. After delivering a surprise 100 bps policy rate hike in late Q1, the Bank of Ghana (BOG) adopted a wait-and-see approach in Q2 amid rapidly easing inflation. At its Monetary Policy Committee meeting on May 23, the BOG held the benchmark rate at 28.0% , choosing to maintain a tight stance to firmly anchor expectations. This decision was well anticipated by markets, given the favourable inflation trend: Ghana’s headline inflation decelerated for a fourth consecutive month in April, coming in at 21.2% (down from 22.4% in March). More impressively, price pressures abated further in late Q2; inflation in May dropped sharply to 18.4% , the lowest level in over three years. Drivers of this disinflation included a stable Ghanaian cedi, lower import costs, and the government’s fiscal restraint under its IMF program. In fact, the cedi enjoyed a remarkable appreciation of about 17% against the US dollar since April, buoyed by Ghana’s tight monetary policy, record-high reserve accumulation, and strict enforcement of forex rules. The currency’s strength materially reduced imported inflation, allowing Ghana to approach the mid-2020s with inflation back on a downward glidepath toward the BOG’s 8% (+/−2) target band. Investor reactions to Ghana’s improving fundamentals were notably positive . Yields on Ghana’s Eurobonds tightened significantly over Q2 as confidence tentatively returned. Ghana’s dollar bonds rallied particularly strongly in May, with one once-distressed issue delivering some of the best returns among emerging-market peers during that month (a stark reversal from its “shunned” status in 2022). Market sentiment was buoyed by both the macro trends and concrete progress on debt matters. The government stuck to its fiscal consolidation plans. Finance Minister Ato Forson’s mid-year budget review affirmed steep spending cuts aimed at narrowing the deficit and projected inflation to fall to ~12% by December. Moreover, Ghana moved closer to restoring its international creditworthiness: having completed its domestic debt exchange and made headway in talks with bilateral creditors, the country received multiple credit rating upgrades , including from Fitch in June (from Restricted Default up to ‘B-’ with a stable outlook). This upgrade, premised on Ghana’s successful IMF program implementation and improved debt trajectory, reinforced the sense that the worst of Ghana’s crisis is over. Nonetheless, challenges remain . Year-end inflation, even if lower, will likely stay above target, requiring the BOG to keep monetary policy tight for an extended period. Any premature rate cuts are unlikely until disinflation is firmly entrenched. Additionally, Ghana must still restructure its outstanding debts (negotiations with private creditors are ongoing), and the outcome will determine its long-term debt sustainability. In sum, Q2 2025 showcased Ghana’s resilience: the economy is slowly stabilizing under disciplined policies, and investors are tentatively rewarding Ghana’s commitment to reform after a turbulent 2024. Kenya In Q2 2025, Kenya’s Eurobond market benefited from improving macroeconomic stability and accommodative monetary policy , even as observers cautioned that structural fiscal issues could pose risks down the line. The quarter brought further easing of interest rates by the Central Bank of Kenya (CBK), a continuation of the dovish pivot begun earlier in the year. Surprising markets, the CBK Monetary Policy Committee cut the benchmark rate twice in Q2: first by 75 bps on April 8 (from 10.75% to 10.00%), and again by 25 bps on June 10 to 9.75% . This marked the fifth and sixth consecutive MPC meetings with a rate reduction, underscoring the CBK’s determination to spur domestic credit and growth. In its June statement, the MPC noted there was “scope for further easing” to support private sector lending, given that inflation remained comfortably within the target range. Indeed, Kenya’s inflation stayed subdued throughout Q2. The annual rate was just 3.8% in June (below the 5% midpoint of the 2.5–7.5% target band), thanks to lower food prices, a stable Kenyan shilling, and prior fuel subsidy impacts fading. With price stability achieved, the CBK’s rate cuts aimed to address Kenya’s other concern: slowing economic momentum in the face of fiscal tightening. The benefits of Kenya’s improved monetary environment were quickly reflected in its Eurobond performance. Yields on Kenya’s sovereign bonds fell notably over the quarter, retracing the risk-premium spike seen late last year. By Q2’s end, Kenya’s 10-year Eurobond yield had declined roughly 100–150 bps from its February highs, as global investors responded to Kenya’s low inflation and proactive policy easing. However, not all indicators were rosy . In May, the World Bank cut Kenya’s 2025 GDP growth forecast to 4.5% (from 5.0%+), citing high public debt and a crowding-out of private credit by government borrowing. Furthermore, Kenya’s public finances remain under strain: debt-to-GDP stands at about 65%, and fiscal consolidation has been uneven due to revenue shortfalls and rising debt service costs. The government in Q2 applied for a new IMF program to shore up confidence and fill financing gaps, after complications with the prior program’s review. Eurobond investors, while heartened by Kenya’s short-term macro improvements (low inflation, current account deficit expected to narrow to just ~1.5% of GDP), are also mindful of these medium-term risks. The remainder of 2025 will test Kenya’s ability to sustain reforms, such as implementing World Bank-advised tax measures to boost revenue, without derailing the growth recovery. For now, in Q2 Kenya struck a constructive balance: policy credibility and easing inflation bolstered its market standing, even as the country worked to address the deeper issues of debt and inclusive growth.

Zambia Zambia emerged in Q2 2025 as a regional bright spot where favourable sectoral trends and steady policy management coexisted with persistent macro challenges. The country’s pivotal copper sector continued to attract significant investor interest and drive economic optimism. Building on the momentum from Q1, major mining companies expanded their commitments in Zambia during the quarter. The $50 million regional exploration campaign underscored Zambia’s central role in the global “copper rush” linked to electric vehicle demand. Likewise, cross-border mining collaboration with the Democratic Republic of Congo deepened, as both countries sought to leverage record-high production. These developments reinforced investor perceptions that Zambia stands to benefit enormously from medium-term commodity trends, potentially boosting exports, government revenues, and FDI inflows. Amid this positive backdrop, Zambia’s policymakers in Q2 demonstrated a commitment to taming inflation and stabilizing the economy . After back-to-back interest rate hikes in late 2024 and February 2025, the Bank of Zambia (BoZ) chose to hold rates steady at 14.50% at its May 23 meeting. The decision to pause further tightening was underpinned by early evidence that inflation was leveling off: annual CPI registered 16.5% in both March and April, essentially plateauing after peaking at 16.8% in February. The central bank revised down its average inflation projection for 2025 to 13.5% (from 14.6%), reflecting expectations that a stable kwacha and prudent fiscal policies would gradually ease price pressures. On the growth front, Zambia received a welcome upward surprise. Thanks to a strong harvest and mining sector resilience in the wake of last year’s drought, the Ministry of Finance upgraded the 2024 GDP growth forecast to 4.0% , a substantial improvement from the mere 1.2% expansion expected earlier. While 2025 growth is still envisioned to benefit from robust copper production, authorities remain cautious given inflation is above target and some fiscal consolidation is needed under Zambia’s IMF program. Zambia’s Eurobonds saw mixed movements over Q2. Early in the quarter, yields widened modestly (by ~30–50 bps) as global risk aversion spiked during the U.S. tariff brinkmanship and the mid-June oil shock – the latter hurt Zambia as a net oil importer. However, by late June, sentiment toward Zambia improved alongside easing global concerns and the country’s encouraging domestic news. Investors were comforted by Zambia’s steady monetary hand and the sense that inflation, though high, is under control and set to fall. For now, investors remain cautiously optimistic . Zambia’s Eurobond prices rallied off their lows and trading volumes picked up as dedicated emerging-market funds speculated on a debt resolution. The country’s commitment to structural reforms (such as overhauling its mining royalties and promoting local value-add in the copper supply chain) has further bolstered confidence. Nevertheless, risks persist, including the need to decisively reduce inflation and to navigate the debt overhaul without delay. In summary, Zambia in Q2 2025 offered a compelling story of long-term potential buttressed by short-term policy credibility . |

Q2 2025 Outlook Local market In the FGN bond and Treasury bills space, we expect the mild bullish sentiments to persist into the new quarter. We further anticipate the progressive reduction of yields in both markets. However, on the back of the over c.N3 trillion expected in coupon payments and bill maturities through the quarter, we anticipate pockets of cherry-picking as participants look to allocate surplus liquidity. Eurobond market

|