Q3 2025 Growth Moderates but Remains Broad-Based

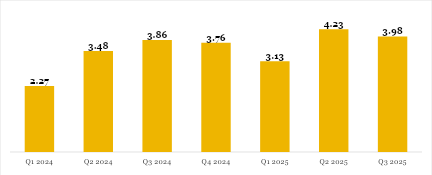

Nigeria’s economic growth remained on a positive trajectory in Q3 2025, although the pace moderated slightly relative to the previous quarter. According to the latest data released by the National Bureau of Statistics (NBS), real GDP grew by 3.98% year-on-year, easing from 4.23% in Q2 2025 but still surpassing the 3.86% recorded in Q3 2024. In nominal terms, total output rose to ₦113.59 trillion, up from ₦101.73 trillion in the preceding quarter and ₦96.16 trillion in Q3 2024, reflecting both output gains and elevated price levels.

The Oil and Non-oil Sector Performance

Oil Sector

The oil sector grew by 5.84% year-on-year, slightly higher than the 5.66% expansion recorded in Q3 2024, but significantly slower than the 20.46% surge posted in Q2 2025. The moderation highlights the volatility of crude oil output and the persistence of operational and security-related constraints. Notably, oil production was down to 1.64 million barrels per day (mbpd) in Q3 2025 from 1.68 mbpd in Q2 2025, but higher than the 1.47mbpd recorded in Q3 2024. The sector contributed 3.44% to real GDP, marginally above the 3.38% recorded a year earlier but below the 4.05% share reported in the previous quarter.

Non-oil Sector

The non-oil sector maintained its steady momentum in the third quarter of 2025, further reinforcing its position as the primary engine of economic expansion. The sector grew by 3.91% in real terms, outperforming both the 3.79% recorded in the same period of 2024 and the 3.64% posted in the second quarter of 2025. This improvement highlights the resilience and broad-based contributions of non-oil activities despite ongoing macroeconomic pressures. Strong performance in agriculture (particularly crop production), financial services, trade, construction, and manufacturing underpinned the sector’s resilience.

The non-oil sector accounted for 96.56% of total real GDP, slightly lower than the 96.62% reported a year earlier but higher than the 95.95% recorded in the previous quarter, reaffirming its dominant role in Nigeria’s growth narrative.