Nigeria’s Economic Growth Slows Slightly to 3.89% in Q1 2026

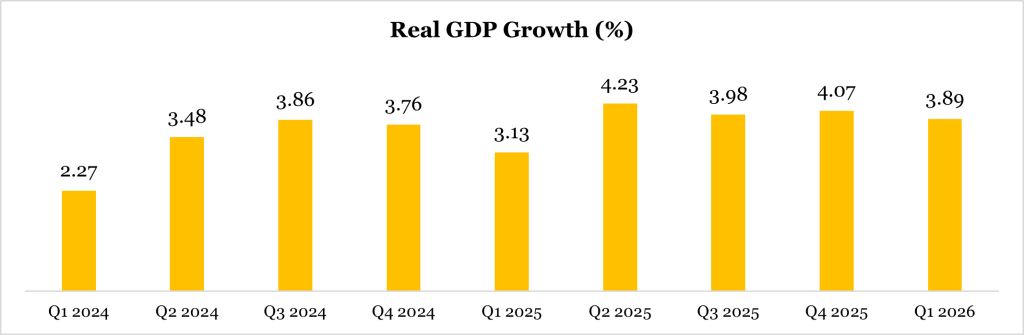

According to the National Bureau of Statistics (NBS), Nigeria’s real GDP grew by 3.89% year-on-year in Q1 2026, slowing from 4.07% in Q4 2025 but improving from 3.13% in Q1 2025, as resilient non-oil activity partly offset weaker oil production. However, the moderation in growth relative to the preceding quarter reflects the typical slowdown in economic activity at the start of the year, alongside persistent pressure on business operating conditions.

Oil and Non-Oil Sector

The oil sector grew by 2.57% in Q1 2026, slowing from 6.79% in Q4 2025, though remaining above the 1.87% growth recorded in Q1 2025. The weaker performance reflected lower crude oil production, with average daily output declining to 1.55 million barrels per day (mbpd) from 1.58 mbpd in Q4 2025 and 1.62 mbpd in Q1 2025, highlighting the persistent impact of crude theft, pipeline vandalism, and operational inefficiencies on oil production. Although the sector contributed 3.92% to total real GDP, up from 2.87% in Q4 2025, Nigeria continues to underperform relative to its oil production potential, constraining fiscal revenues and foreign exchange inflows.

The non-oil sector remained the main driver of aggregate growth, expanding by 3.94% in Q1 2026 compared with 3.99% in Q4 2025 and 3.19% in Q1 2025. With a 96.08% share of total real GDP, the sector continued to anchor overall economic performance, supported by stronger activity in telecommunications, construction, financial services, trade, and oil refining. Increased digital penetration, public infrastructure spending, and stronger domestic refining activity were the key growth supports during the quarter.

Sectoral Breakdown

Of the 46 economic activities tracked by the NBS, 20 expanded, 17 slowed, and 9 contracted in Q1 2026. Key expanding activities included:

| Sector | Q4’2025 | Q1’2026 | Comments |

|---|---|---|---|

| Oil refining | 12.33% | 37.46% | Improved operational activities at Dangote refinery supported growth. |

| Telecoms | 8.39% | 12.24% | Increased usage of data and voice services, reflecting deeper digital penetration and rising demand for internet connectivity. |

| Construction | 5.08% | 6.38% | Increased public sector construction activities boosted demand for cement and other building materials. Cement manufacturing expanded by 11.53% in Q1 2026. |

| Trade | 2.00% | 2.08% | Improved exchange rate stability supported trading activities, although rising logistics and operating costs continued to constrain stronger expansion. |

| Financial institutions | 7.08% | 8.40% | Elevated interest rates and stronger financial intermediation supported earnings growth and sector expansion. |

| Key slowing and contracting activities included: | |||

| Crop production | 3.94% | 3.39% | Persistent insecurity in food-producing regions and rising logistics costs continued to weaken agricultural productivity and food supply. |

| Real estate | 3.43% | 2.29% | Weak consumer purchasing power, elevated building material costs, and high borrowing rates constrained housing demand and property development. |

| Road transport | 23.86% | 9.64% | Rising insecurity, kidnapping incidents, and higher transportation costs weakened passenger and logistics activities. |

| Air transport | 15.17% | -7.62% | Higher aviation fuel prices increased airfares and weakened consumer demand for air travel. |

| Electricity | 4.26% | -15.30% | Lingering structural issues in the power sector and grid instability continued to constrain electricity supply and industrial productivity. |

Outlook

We expect real GDP growth to remain positive in Q2 2026, although the momentum may soften as geopolitical tensions in the Middle East continue to exert upward pressure on global energy prices and domestic operating costs. The main support factors should remain stronger refining activity, continued expansion in telecommunications, and sustained growth in financial services. However, persistent insecurity, elevated inflation, weak consumer purchasing power, and structural bottlenecks in key productive sectors pose significant downside risks to the outlook.