Inflation Sustains its Downward Trend, but Monthly Pressures Re-emerge

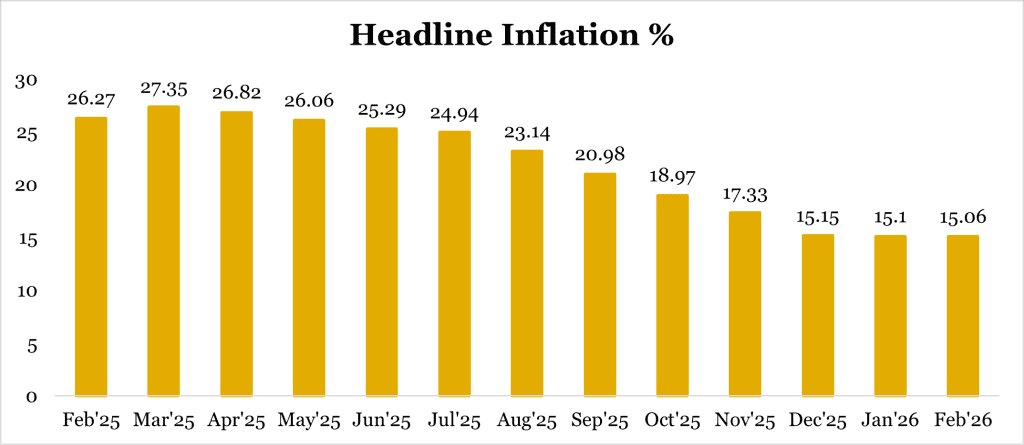

Nigeria’s inflation trajectory continued its gradual descent in February 2026, with headline inflation moderating marginally to 15.06% year-on-year, from 15.10% in January. This marks the eleventh consecutive monthly decline, reinforcing the narrative that the economy remains on a disinflation path.

However, beneath this improving headline figure lies a more nuanced reality. While the moderation reflects improving macroeconomic conditions, particularly exchange rate stability, the slow pace of decline suggests that the economy may be approaching an inflection point. More importantly, the recent rally in global oil prices, with early signs of pass-through to domestic fuel prices, coupled with a sharp rebound in month-on-month inflation, suggests that underlying price pressures are rebuilding, pointing to renewed cost pressures on consumers and businesses. On a month-on-month basis, inflation rose sharply to 2.01%, reversing the -2.88% deflation recorded in January.

Currency Stability Supports Core Inflation

At the heart of the disinflation story is the moderation in core inflation to 15.88% in February from 17.12% in January, largely driven by improved exchange rate dynamics. In February, the Naira appreciated both in the official and parallel markets, gaining 1.70% at the official window and 6.73% in the parallel market. This appreciation has helped to ease imported inflation pressures, particularly across non-food categories.

Food Inflation Surges as the Planting Season Begins

In contrast to the moderation in core inflation, food inflation has reversed course, climbing to 12.12% in February, after briefly dropping to single digits for the first time in over a decade (8.89% in January). This increase underscores the combined impact of persistent structural challenges, Ramadan, seasonality effect. As the planting season begins, supplies typically tighten, driving price increases. This seasonal pattern is further exacerbated by higher logistics costs, insecurity in key food-producing regions, and ongoing inefficiencies across the agricultural value chain. The resurgence in food inflation highlights a critical issue that Nigeria’s inflation is increasingly supply-driven, making it less responsive to improvements in monetary conditions alone.

Inflation Outlook: Risk of Reversal in March

The disinflation trend appears increasingly fragile, with early signals suggesting a potential reversal in March 2026. While exchange rate stability has supported the recent moderation in headline inflation, emerging pressures, particularly from the energy and food segments, are beginning to offset these gains. The recent uptick in global oil prices is expected to transmit into higher domestic fuel costs, with broad-based implications for transportation, logistics, and production costs.

At the same time, the seasonal uptick in food inflation associated with the planting season is likely to intensify in the coming months, further exerting upward pressure on prices. Given the weight of food in the inflation basket, this could materially alter the trajectory of headline inflation.

Policy Implications: Limited Room for Monetary Easing

The February inflation data presents a delicate balancing act for policymakers. While the easing in headline and core inflation provides some room for optimism, the resurgence in monthly price pressures suggests that inflation is not yet fully under control. Additionally, emerging risks from energy prices and food inflation reinforce the need for caution.

As a result, the Central Bank is likely to maintain a tight or neutral monetary policy stance in the near term, prioritizing price stability over aggressive growth stimulation.