Nigeria’s Growth Strengthens in Q4 2025 on Improved Macro Stability

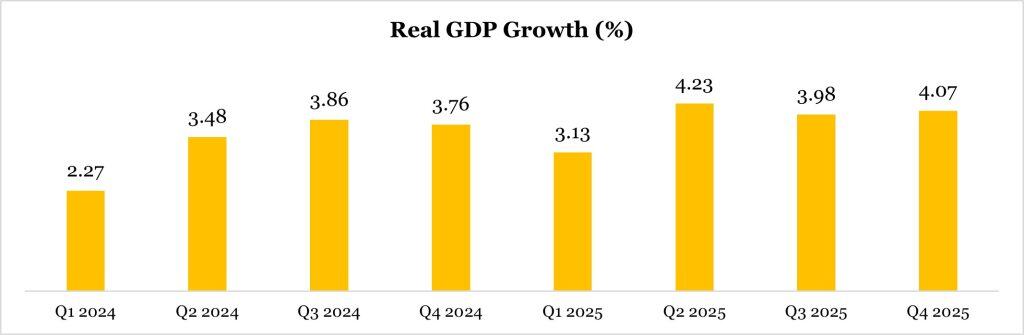

Nigeria’s economy gained further traction in the fourth quarter of 2025, with real GDP expanding by 4.07% year-on-year, marginally higher than the 3.98% recorded in Q3 2025 and above the 3.76% achieved in the corresponding quarter of 2024. As a result, full-year 2025 growth accelerated to 3.87%, compared with 3.38% in 2024.

The resilience in growth momentum reflects more than a cyclical rebound; it underscores the impact of a gradually stabilizing macroeconomic environment. Given Nigeria’s strong exchange rate sensitivity and reliance on imported inputs, the appreciation of the Naira in Q4 2025 significantly reduced imported costs. A firmer currency lowers input expenses for manufacturers and traders while improving pricing visibility, allowing businesses to rebuild margins and manage inventories more efficiently.

At the same time, sustained disinflation supported both households and corporates. Slower price growth improved real purchasing power and boosted aggregate demand, while also reducing operating cost volatility for businesses.

Oil sector

The oil sector recorded improved performance in Q4 2025, expanding by 6.79% year-on-year, up from 5.84% in Q3 2025 and significantly higher than 2.08% in Q4 2024. For the full year, the sector grew by 8.50% in 2025, compared with 5.54% in 2024.

The recovery was largely driven by higher crude oil production, which rose to an average of 1.58mbpd in Q4 2025 from 1.54mbpd in Q4 2024, although it was slightly below Q3 levels. While the sector’s contribution to real GDP remains modest at 2.87%, improved output strengthened export earnings, fiscal revenues, and foreign exchange inflows.

The non-oil sector

The non-oil sector grew by 3.99%, higher than 3.80% in Q4 2025 and 3.91% in Q3 2025. The sector remains a major driver of growth, contributing 97.13% to GDP, higher than 96.56% in Q3 2025 but lower than 97.2% in Q4 2024. This was supported by improved performance in information and communication, financial services, trade, and transportation sectors.

Sector Performance – 26 Expanded, 18 Slowed, and 2 Contracted

Of the 46 economic activities tracked by the National Bureau of Statistics (NBS), 26 recorded an expansion in Q4, 18 experienced a moderation in growth, while only two sectors contracted, underscoring a broadly positive but uneven growth profile across the economy.

Among the expanding sectors were agriculture (4.0%), trade (2.0%), telecommunications (7.55%), and transportation (21.25%). Agriculture continued to benefit from improved crop output and relative stability in input costs, while trade activity was supported by moderating inflation and stronger consumer demand. The telecommunications sector maintained its structural growth momentum, reflecting sustained data penetration and digital adoption, while transportation growth was buoyed by lower energy prices.

Conversely, several sectors recorded a slowdown in growth compared to the prior period. Manufacturing (1.13%) faced lingering cost pressures and capacity constraints despite improved currency stability. Construction (5.08%) also moderated, potentially reflecting slower capital expenditure momentum. Real estate (3.43%) growth eased amid cautious investment sentiments, while financial services (8.3%) decelerated, partly due to the tight monetary policy stance.

Outlook

We expect Nigeria’s GDP growth to moderate in Q1, reflecting the typical seasonal lull in economic activity at the start of the year. Historically, first-quarter output tends to soften as post-festive demand normalizes.

However, while sequential momentum may ease, underlying macro conditions remain supportive. The sustained appreciation of the Naira is expected to continue easing imported cost pressures, improving business confidence and margin stability. At the same time, the ongoing moderation in inflation should help preserve consumer purchasing power and support real sector activity.

The MPC’s gradual shift toward monetary easing is also likely to gradually improve liquidity conditions and lower financing costs albeit marginally, providing incremental support to credit-sensitive sectors.

In addition, elevated oil prices, driven by escalating tensions in the Middle East, should bolster export earnings and fiscal revenues, reinforcing foreign exchange stability and external buffers. While the direct GDP contribution of oil remains modest, the secondary effects through improved FX liquidity and government spending capacity could provide meaningful macro support.