The quarter opened with bearish bias on the back of system illiquidity. This bias continued post first auction, as players took profit especially on the new 1-year paper. However, pockets of demand emerged towards the end of April-2024 as participants looked to take advantage of the market levels. The second month started out with bullish sentiments amid scarce offers as players took on a cautious stance while anticipating the outcome of the MPC meeting. Following the MPC decision and FAAC inflow, demand intensified amid some profit taking activities. In the last month of the quarter, mixed sentiments were witnessed albeit, with a bearish tilt. Mid- month, we witnessed a bit of cherrypicking, albeitthe quarter closed out with the bears taking the centre stage. Q-o-Q, yields increased by an average of c.230bps across the Jul’24-Feb’25 maturities.

The CBN floated seven OMO auctions during the quarter offering c.N3.05trn across the standard tenors. Sales through the quarter was about N2.0trn despite the oversubscriptions recorded at the auctions. Worthy of note is the no sale recorded at the penultimate auction floated in the quarter despite the N321.5b subscription.

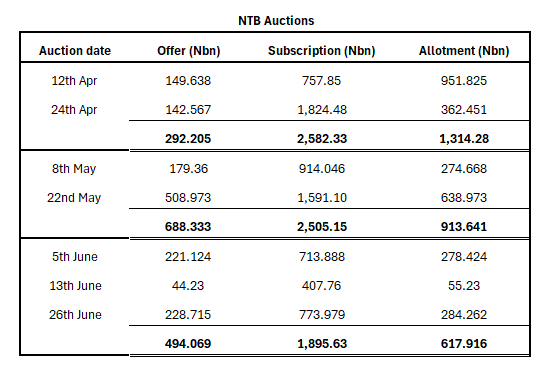

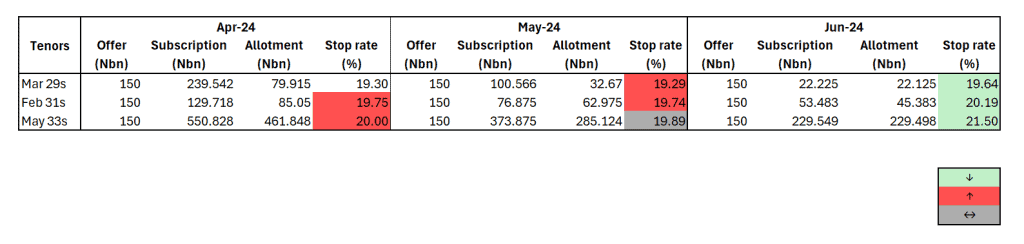

The DMO conducted seven auctions through the quarter with each month recording about 8x . 3.6x, 3.8x oversubscription respectively. In total, the FG oversold c.N1.37trn across the standard tenors. Stop rates remained relatively stable through the quarter, however closing at 16.30% (vs. 16.24% Q1 ending), 17.44% (vs. 17.00% Q1 ending) and 20.68% (vs. 21.124% Q1 ending).