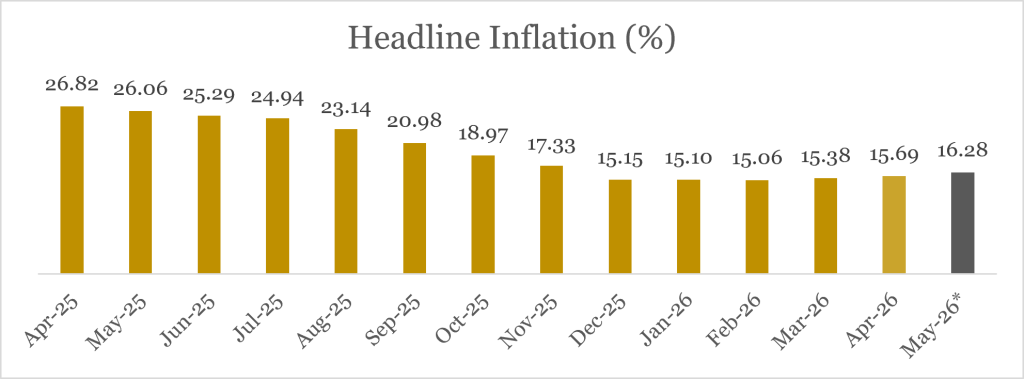

Inflation Projected to Rise to 16.28% in May

The Middle East crisis has materially altered inflation dynamics, not only in Nigeria but across the global economy. Disruptions to energy supply chains and the resulting increase in crude oil prices have renewed inflationary pressures across both advanced and emerging markets, interrupting the disinflation trend that had gained traction earlier in the year. Higher energy costs have filtered through transportation, production, and logistics channels, resulting in broader consumer price pressures and renewed concerns over inflation persistence.

The impact is already visible across major economies. In the United States, inflation accelerated sharply to 4.2% in May from 2.4% in February, reflecting the pass-through effect of higher energy prices and broader cost pressures. Across Africa, inflationary conditions have also remained elevated as economies continue to contend with higher fuel prices. Inflation in Kenya and Ghana climbed to 6.7% and 3.7% in May from 4.3% and 3.3% in February, highlighting the increasingly global nature of current inflation pressures and the vulnerability of emerging markets to external shocks.

Nigeria has not been insulated from these developments. After recording eleven consecutive months of moderation, headline inflation reversed course in March and increased further to 15.69% in April, reflecting the transmission of higher energy costs into domestic prices. The annual price index is expected to increase further to 16.28% in the month of May when the NBS releases its data next week (June 15).

However, a closer assessment of the inflation profile suggests that underlying price pressures may not be accelerating at the same pace as the headline figure implies. Month-on-month inflation moderated to 2.13% in April following the sharp increase recorded in March and is projected to ease further to 2.05% in May, suggesting that the immediate pass-through effect of the oil price shock may be gradually fading.

Although festive periods typically support stronger consumer demand and higher prices, the expected impact of the Eid-Adha celebrations appears to have been moderated by weak consumer purchasing power, limiting the extent of price pass-through during the review period.

Consequently, while headline inflation is expected to remain elevated due to lingering base effects, the moderation in the monthly inflation index suggests that underlying inflation momentum may be easing. Looking ahead, the recent downward adjustment in PMS pump prices following the reduction in Dangote Refinery’s gantry price could provide some relief to transportation and distribution costs, helping to moderate broader second-round inflation effects across the economy.

Rising Insecurity to take a significant toll on Food Inflation

Food inflation is expected to remain under pressure due to worsening insecurity across key agricultural regions. Persistent security challenges continue to disrupt farming activities and limit the movement of agricultural produce from farm clusters to major consumption centres. These disruptions, combined with elevated logistics costs, are likely to sustain upward pressure on food prices and offset some of the gains from recent moderation in energy costs.

Conclusion

Overall, the expected increase in inflation appears to reflect the lingering energy-related base effects. Going forward, greater attention should be placed on month-on-month inflation dynamics and food inflation trends, as these indicators are likely to provide a clearer signal on whether current pressures are becoming entrenched or remain temporary in nature.