Inflation Moderates as Core Inflation Eases, But Geopolitical Risks Cloud the Outlook

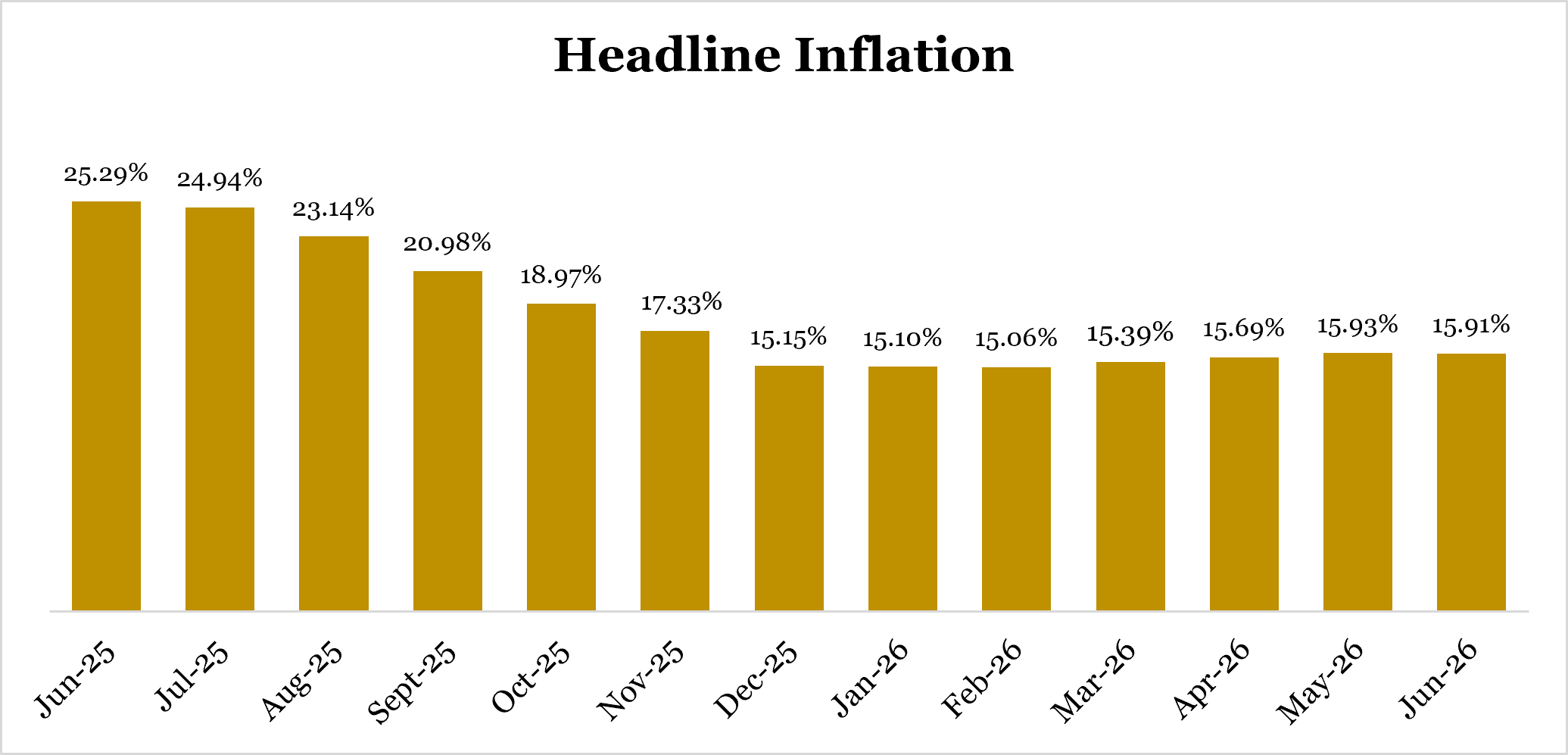

Nigeria’s headline inflation moderated marginally to 15.91% year-on-year (y/y) in June 2026 from 15.93% in May, broadly in line with our forecast of 15.88%. The outturn marks the first moderation following three consecutive months of increases, suggesting that inflationary pressures eased modestly during the month. Consistent with this trend, month-on-month inflation slowed to 1.66% from 1.75% in May, indicating a slower pace of increase in consumer prices.

Core Inflation Drives the Decline in Headline Inflation

The moderation in headline inflation was driven primarily by a sharp slowdown in core inflation to 15.92% y/y from 16.82% in May. This largely reflected the easing in global energy prices following the ceasefire between Israel and Iran in late June, which reduced concerns over potential supply disruptions in the Middle East. The subsequent decline in crude oil prices, alongside successive reductions in domestic petrol prices, helped lower transportation and logistics costs, easing cost pressures on businesses and households.

In addition, the relative stability of the foreign exchange market during the review period helped contain imported inflation by limiting the pass-through of exchange rate movements to domestic prices. The naira appreciated by 0.47% during the month to close at ₦1379.68/$, further supporting the moderation in core inflation.

Food Inflation Remains the Achilles’ Heel

Despite the improvement in core inflation, food inflation accelerated to 17.52% y/y from 16.96% in May, highlighting the persistence of structural supply-side constraints. Insecurity across key food-producing regions, weather-related disruptions associated with the rainy season, elevated transportation costs in some parts of the country, and distribution bottlenecks continued to exert upward pressure on food prices.

The continued acceleration in food inflation suggests that Nigeria’s inflation challenge remains largely structural. Until these bottlenecks are addressed, food prices are likely to remain elevated, limiting the pace of headline disinflation.

June’s Improvement May Be Temporary

While the June inflation print is encouraging, we caution against interpreting it as the beginning of a sustained disinflation trend.

The moderation in inflation largely reflected temporary relief from lower global oil prices following the Middle East ceasefire. However, the recent re-escalation of geopolitical tensions has renewed concerns over disruptions to global oil supply and the prospect of higher energy prices. Should the conflict intensify or persist, rising crude oil prices could feed through to higher domestic fuel prices, transportation costs and imported inflation, potentially reversing the gains recorded in June.

Consequently, we view the June moderation as potentially a blip rather than the start of a sustained disinflation trend, particularly as food inflation continues to accelerate and domestic structural constraints remain unresolved.

Beyond geopolitical risks, inflationary pressures remain elevated due to persistent insecurity in food-producing areas, adverse weather conditions, high logistics costs, infrastructure deficiencies and the recent depreciation of the naira, partly reflecting seasonal foreign exchange demand associated with summer travel and overseas school fees.

MPC Likely to Remain on Hold

Against this backdrop, we expect the Monetary Policy Committee (MPC) to maintain its cautious policy stance at its next meeting. While the moderation in headline inflation provides tentative evidence that price pressures may be easing, policymakers are unlikely to interpret a single month’s decline as sufficient confirmation that inflation has been brought under control.

The continued acceleration in food inflation, coupled with renewed geopolitical uncertainty and emerging exchange rate pressures, is likely to reinforce the Central Bank of Nigeria’s commitment to preserving price and exchange rate stability. Accordingly, we expect the MPC to leave the Monetary Policy Rate (MPR) unchanged while monitoring whether the moderation in core inflation proves durable over the coming months.

Market Implications

Fixed Income: Higher-for-Longer Rate Environment Supports Yields

We expect the MPC’s decision to maintain the current policy rate to reinforce the higher-for-longer interest rate environment. Although the June inflation print modestly improves real yields, the combination of persistent food inflation, heightened geopolitical risks and the Federal Government’s sizeable borrowing programme suggests that domestic yields are likely to remain elevated.

Treasury bill and FGN bond yields are therefore expected to remain broadly stable in the near term, supported by continued tight monetary policy and robust supply from government borrowing. This environment should sustain investor demand for fixed income securities, particularly among pension funds and other institutional investors seeking attractive real returns.

Equities: Selective Positioning to Persist

For the equities market, an unchanged policy rate implies that financing conditions will remain relatively tight, limiting the scope for a broad-based re-rating of equity valuations. Elevated interest rates also preserve the attractiveness of fixed income instruments, which could temper portfolio rotation into equities.

Nevertheless, the moderation in core inflation is expected to provide some relief to companies by easing transportation, logistics and imported input costs. Consequently, investor interest is likely to remain concentrated in fundamentally strong companies with resilient earnings, solid pricing power and robust balance sheets, particularly within the banking, industrial and selected consumer goods sectors.