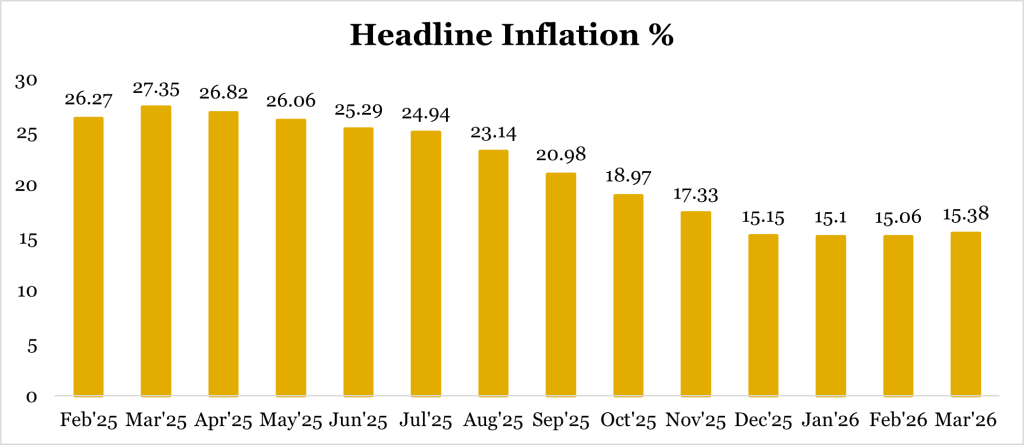

Inflation Bucks its 11-month declining trend (15.38%)

The March 2026 CPI published by the National Bureau of Statistics signals a clear turn in Nigeria’s inflation trajectory, with headline inflation recording its first increase after eleven consecutive months of decline. This marks an early indication of a re-emergence of underlying price pressures and a break from the recent disinflationary path.

Headline inflation rose by 0.32% to 15.38% year-on-year (February: 15.06%), broadly in line with our forecast of 15.39%. While the increase in the annual index remains moderate, largely reflecting favourable base effects, the underlying momentum is more evident in monthly trends. Month-on-month inflation surged to 4.18% from 2.01%, pointing to a sharp re-acceleration in current price pressures.

This increase was largely driven by the pass-through from higher energy costs, particularly the adjustment in Premium Motor Spirit (PMS) prices linked to geopolitical tensions in the Middle East, with immediate spillovers into transportation and logistics costs.

Core Inflation up as Energy-Driven Pressures Intensify

Core inflation rose to 16.21% year-on-year, up by 0.33% from 15.88% in February. On a monthly basis, it climbed sharply to 4.03% from 0.89%, largely reflecting energy-driven price pressures.

Food Inflation Moved in Varied Direction

The annual and monthly food inflation sub-indices moved in varied directions. While year-on-year food inflation rose to 14.31% from 12.12% in February, the month-on-month food subindex moderated to 4.17% from 4.69%, partly supported by consumer price resistance and weak aggregate demand.

Outlook

Inflation is expected to edge higher in the coming months, largely driven by elevated energy costs. However, recent fiscal interventions could offer some medium-term moderation. In particular, the planned tariff reductions on over 100 items, including key food commodities, alongside zero import duties on agricultural and industrial machinery, are likely to ease supply bottlenecks and reduce production costs over time.

The Monetary Policy Committee (MPC) is scheduled to meet on May 19–20, with the March inflation uptick set to be a key consideration. Importantly, April inflation data will also be available ahead of the meeting, providing a clearer basis to determine whether the March increase was a transitory shock or indicative of a more sustained inflationary trend. Overall, we expect the MPC to remain data-dependent, with a bias towards maintaining a tight monetary stance.